Charge-Offs on Your Credit Report: Can You Remove Them? (FL Guide)

How to Remove a Charge-Off From Your Credit Report (Orlando Credit Repair Guide)

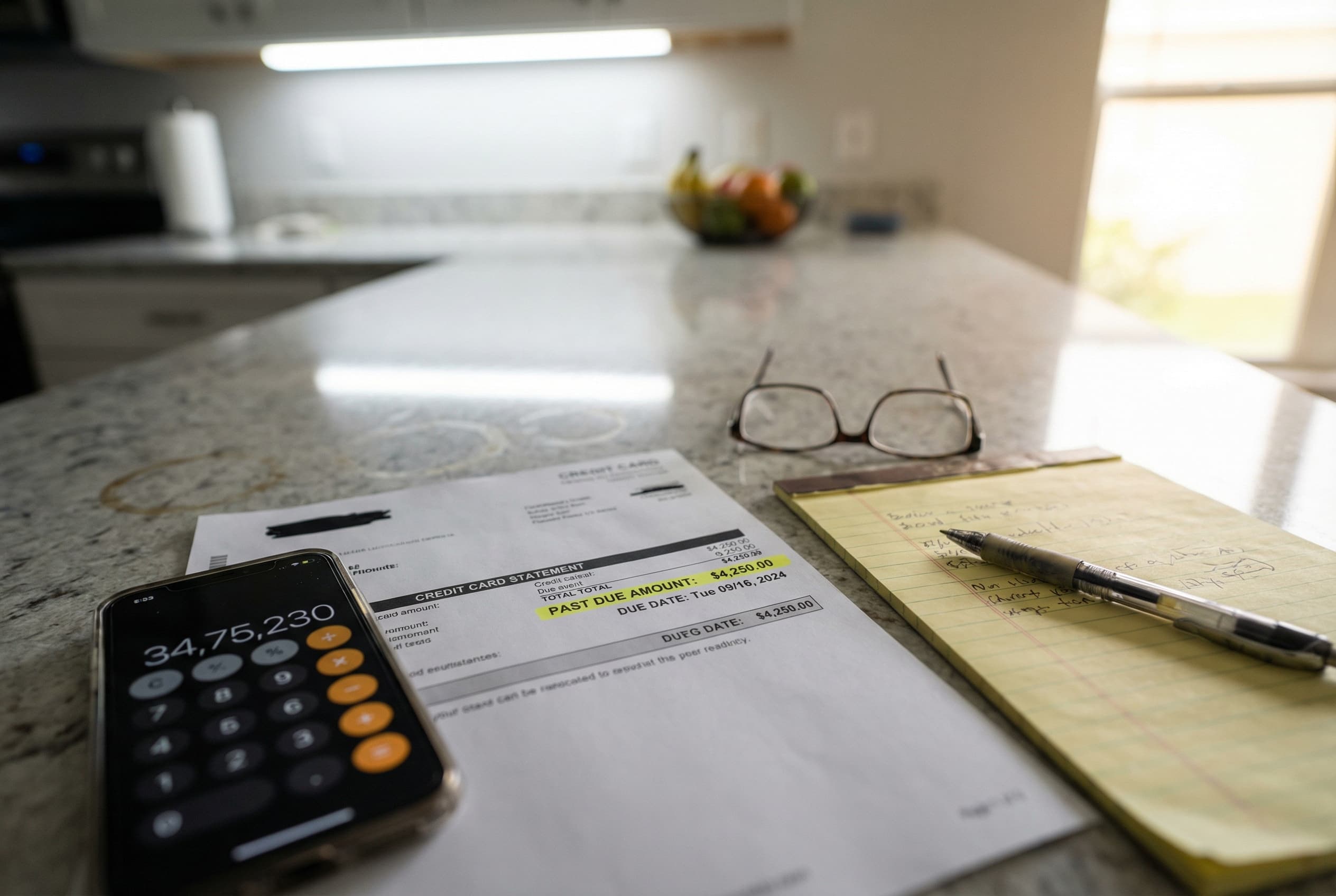

You just pulled your credit report and there it is — a charge-off sitting there like a giant red stain. Maybe it's a credit card you fell behind on two years ago. Or maybe life just blew up on you — divorce, job loss, medical emergency — and honestly, paying some credit card bill was the absolute last thing on your radar.

I've been there with clients. I've been doing [INTERNAL_LINK:credit repair in Orlando] for 20 years, and I see charge-offs on reports every single day.

But look, I need you to hear this before you do anything else: a charge-off is NOT the same as a collection. Treat it the same way and you're gonna make things worse — trust me, I've watched it happen more times than I can count. I've watched people tank their own chances of getting that charge-off removed because they did things in the wrong order or believed bad advice from some Reddit thread.

So let me break down what's actually happening here and exactly what you should do about it — step by step, no fluff.

TL;DR: A charge-off isn't a death sentence — but it's harder to remove than a collection. The winning strategy? Find reporting errors, pay it off (negotiate those junk fees down), then dispute. Keep reading for the full play-by-play, including Florida-specific rules that could save your skin.

What a Charge-Off Actually Means (And Why It's Not What You Think)

A charge-off doesn't mean the debt disappeared. It doesn't mean the creditor "gave up." It means the original creditor — Chase, Capital One, Discover, whoever — decided to write your account off as a loss for their accounting purposes. That's literally all it is. A bookkeeping move on their end.

You still owe the money.

The creditor reports the account as "charged off" to Equifax, Experian, and TransUnion. And that status stays on your credit report for 7 years (plus up to 180 days) from the Date of First Delinquency (DOFD) — the first missed payment that triggered the account closure. Not 7 years from when you noticed it. Not 7 years from when they sold the debt. From that original missed payment date.

I had a client in Kissimmee last year who thought the clock reset when Capital One sold his debt to a collection agency. It doesn't. The DOFD is what matters under the FCRA.

Here's the thing — a single charge-off can drop your score 100+ points depending on your profile. Trying to buy a home in Orlando right now? That charge-off is gonna make your mortgage lender very, very nervous.

What Happens If You Ignore It

OK so here's a real scenario — let me show you what this actually looks like.

Imagine "Maria" in Winter Park has a $1,200 charged-off credit card from 2021. She figures, it's already on my report, what's the point? So she ignores it.

And here's where it all goes sideways:

- The original creditor sells the debt to a collection agency. Now Maria has both a charge-off AND a collection on her report for the same debt. Double damage.

- The collection agency starts calling. And if they violate the FDCPA while doing it (the FDCPA covers most third-party collectors, not usually the original bank), that's a separate issue — but most people don't know their rights well enough to catch it.

- Her credit score keeps bleeding. As long as that charge-off reports with a balance or unpaid status, it can keep her scores suppressed.

- She gets denied for the apartment she wanted in Baldwin Park. Landlords pull credit in Orlando. They see a charge-off and move on to the next applicant.

Doing nothing is a choice. And honestly? It's almost always the choice that costs you the most.

So can you just ride it out and wait? I mean, technically — sure, you can. After 7 years from that first missed payment — with no payment made by you in between — the charge-off should fall off your credit report.

But here's the kicker: they don't rush to delete it on their end. I've seen charge-offs hang around for 7 years and 3 months, 7 years and 6 months, because the creditor or the bureau just... didn't bother. You might have to dispute it yourself to force the removal once that 7-year window closes.

So even the "do nothing" approach requires action eventually.

Can You Actually Remove a Charge-Off From Your Credit Report?

Real talk — charge-offs can sometimes be deleted. But I've found that charge-offs are significantly harder to delete than collections. And I need you to understand why, because the strategy is completely different.

With a collection account, you can often negotiate a pay-for-delete with the collection agency. They're third-party buyers who purchased your debt for pennies on the dollar. They have financial incentive to work with you.

A charge-off? That's reported by the original creditor — a bank, a credit card company. These are massive institutions with rigid reporting policies. They don't do pay-for-delete like a collection company would. Seriously — I need you to burn this into your brain. I've had clients call up Bank of America and say, "I'll pay this in full if you delete it," and the rep literally doesn't have a button for that.

So how do charge-offs actually get removed? Usually through one of these paths:

Path 1: Errors on the Reporting

Honestly, this is hands down the most effective route I've seen — and I've been doing this for 20 years, so that's saying something. Under the FCRA Section 611, you've got the right to dispute anything on your credit report that's inaccurate, incomplete, or unverifiable. That's the law.

And guess what? Charge-offs are riddled with errors. I'm talking:

- Wrong balance amounts (this one is huge — more on that in a sec)

- Incorrect dates of first delinquency — if they report the wrong date, the entire 7-year timeline is off

- Account listed as "open" when it should be "closed"

- Wrong account number or creditor name after the debt was sold

- Missing payment history that should show prior on-time payments

- Duplicate reporting — the charge-off AND a collection showing as two separate debts for the same account

If you find ANY of these errors, you dispute it. The bureau has 30 days to investigate under the FCRA (up to 45 if you provide additional info during that window), and if the creditor can't verify the exact information, the bureau should delete it.

I had a client in Dr. Phillips whose $4,200 Discover charge-off got removed because the balance reported didn't match Discover's own records. One number was off. Gone.

Path 2: Pay It Off, THEN Dispute

OK so here's where the order of operations matters and where most people screw up.

If you're going to pay off a charge-off — especially if you're preparing for a mortgage — do NOT dispute it before you pay it. That makes the whole process harder. The creditor is more defensive about accounts with open disputes, and you lose leverage. (Also, heads up: if you're actively mortgage-shopping, many lenders want disputes removed or closed before they'll underwrite your loan. Talk to your lender before opening any disputes.)

Here's the sequence I tell every client at Freedom Credit Repair:

First — Pay it off (and negotiate the amount — I'll explain how below) Next — Wait for the account to update to "Paid Charge-Off" Then — Dispute for errors or inaccuracies

A "Paid Charge-Off" is better than an unpaid one for your score, but it's still ugly. The good news? Once it's marked as paid, the original creditor has less motivation to fight a dispute. They got their money. They've moved on — you're not on their radar anymore. If the bureau sends them a verification request and they don't respond within the investigation window? It should be deleted.

One important note: If you're NOT buying a home and the reporting has clear errors, you can absolutely dispute first based on inaccuracies alone — without paying a cent. Path 1 is its own standalone strategy. This pay-then-dispute path is specifically powerful when you need to satisfy a lender AND clean up the report.

Path 3: Wait Out the Clock (But Force the Deletion)

If the charge-off is already 5-6 years old and you haven't made any payments on it, sometimes the smartest play is to run out the clock. After 7 years from the Date of First Delinquency, it has to come off.

But like I said — don't assume it'll happen automatically. Dispute it the moment that 7-year mark hits. I keep a calendar for my clients' accounts, and we file disputes the week after expiration. The bureaus will drag their feet if you let them.

Look, if you're reading this and your head is already spinning — I hear you, and you're not the only one. This stuff is complicated, and the stakes are high. If you want us to handle this for you, [INTERNAL_LINK:schedule a free consultation] — we'll review your reports and map out a game plan.

The Hidden Trap: Fines and Fees They Stack on Your Charge-Off

This one makes my blood boil, and almost nobody out there is talking about it.

Once a creditor charges off your account, they don't just freeze the balance. They tack on late fees, penalty interest, over-limit fees, and other fines after the account is closed. I've seen a $300 credit card balance balloon to $700+ by the time the client calls to pay it off.

Seven hundred dollars. On a card that had a $300 balance. (I wish I was kidding.)

Here's what you need to know: those fines and fees are generated by an algorithm. There's no human sitting in an office manually calculating your penalties. It's automated. A computer added those charges.

And because there's no human labor behind those fees, creditors are often willing to waive them if you ask.

When you call to settle or pay off a charge-off, say this:

"I'd like to pay what I originally owed on this account. Can you remove the fees and penalties that were added after the account was closed?"

Honestly, I'm still shocked by how often they just say yes. I've had clients in Orlando settle $700 charge-offs for $300 — the original balance — just by asking. The worst they can say is no. But they often say yes because they'd rather get $300 today than chase you for $700 they might never collect.

Get any agreement in writing before you pay a dime. Email, letter, fax — I don't care. Just get it documented.

The Step-by-Step Action Plan to Remove a Charge-Off

OK, so if you were sitting across from me right now at my office here in Orlando, coffee in hand — here's exactly what I'd tell you to do:

Step 1: Pull All Three Credit Reports

Hit up AnnualCreditReport.com — pull your Equifax, Experian, and TransUnion reports, all three of them. The charge-off might show up differently on each one — different balances, different dates, different statuses. That's actually good for you, because inconsistencies are disputable errors.

Step 2: Document Everything About the Charge-Off

Write down:

- Creditor name

- Account number

- Balance reported on each bureau

- Date of first delinquency on each bureau

- Account status (open, closed, paid, unpaid)

- Whether a collection account also appears for the same debt

Step 3: Check the Age

If it's been close to 7 years since your first missed payment (not the charge-off date — the first missed payment that led to the charge-off), you might be better off waiting and then disputing for removal once the time expires.

Still 3-4+ years away from that 7-year mark? Then sitting around waiting doesn't make sense — you need to get aggressive and take a more active approach.

Step 4: Decide — Pay or Don't Pay

If you're buying a home soon: Most mortgage lenders in Central Florida want charge-offs either paid or explained. An FHA lender might require payoff. So paying might be unavoidable.

If you're not in a rush: You might dispute first based on reporting errors alone, without paying. Got inaccuracies on the reporting? You don't owe them a single cent to get that thing removed.

If you decide to pay: Call the creditor and negotiate the amount. Ask to pay the original balance without fines and fees. Get the agreement in writing. Pay it. Wait for the report to update. THEN move to disputes.

Step 5: File Your Disputes

Send dispute letters to the credit bureaus identifying specific inaccuracies. Not a vague "this isn't mine" — specific errors.

- "The balance reported is $724, but my original balance was $312."

- "The date of first delinquency is listed as March 2020, but my last on-time payment was January 2020."

- "This account is reported as open, but it was charged off and closed in 2019."

Under FCRA Section 611, the bureau has 30 days to investigate (up to 45 if you submit additional info). If the creditor can't verify the exact information, the item should be removed.

Step 6: Follow Up Aggressively

Don't send one dispute and sit back. If the bureau comes back and says "verified," you have the right to request their method of verification under FCRA Section 611. Send that request. Make them prove it.

I've seen accounts get removed on the second or third dispute after the creditor finally doesn't respond. Persistence wins here.

Step 7: Consider Professional Help

Look, I'm biased — I own a credit repair company. But I also know that disputing charge-offs is harder than disputing collections, and the margin for error is smaller. If you file a sloppy dispute or do things in the wrong order, you can actually make the situation worse.

If you're in the Orlando area and you want someone to handle this for you, that's literally what we do at [INTERNAL_LINK:our credit repair services]. We've removed charge-offs for hundreds of clients across Central Florida. (Results vary — we can't guarantee deletions, but we know where to find errors and how to fight them the right way.)

Book Your Free Credit Consultation

Take the first step toward better credit. Our experts are ready to help you in Orlando and across Florida.

Charge-Off vs. Collection: Why the Strategy Is Different

I need to hammer this home because I get calls every week from people who tried to handle their charge-off like it was a collection.

| Collection | Charge-Off | |

|---|---|---|

| Reported By | Third-party debt buyer | Original creditor (bank, card company) |

| Pay-for-Delete? | Often possible | Almost never |

| Negotiation Leverage | High — they bought the debt cheap | Lower — they're a big institution |

| Best Removal Strategy | Negotiate deletion, dispute errors | Dispute errors, pay then dispute |

| Typical Difficulty | Moderate | Hard |

See the difference? With a collection agency, you're negotiating with someone who bought your $2,000 debt for maybe $200. They'll take $800 and agree to delete. Everybody wins.

With a charge-off, you're dealing with Chase or Citi or whoever. They don't do pay-for-delete. Their compliance departments have strict reporting policies. So the angle is almost always accuracy-based disputes, not negotiation.

That's why the order matters so much. Pay it off, get it updated, then attack the reporting for errors.

Want to understand the differences between charge-offs and collections even deeper? Check out [INTERNAL_LINK:our guide on dealing with collection accounts].

What About "Goodwill Letters" for Charge-Offs?

You've probably seen people online recommend sending a "goodwill letter" asking the creditor to remove the charge-off out of the kindness of their heart.

Honestly? In my experience, these almost never work for charge-offs. I've seen them work occasionally for a late payment on an otherwise perfect account. But a charge-off? That's the creditor saying you defaulted so badly they wrote you off. A goodwill letter asking them to pretend that didn't happen is a long shot.

Is it worth trying? Sure, it costs you a stamp. But don't build your strategy around it.

Florida-Specific Things You Should Know

Florida has a 5-year statute of limitations on credit card debt under Florida Statute 95.11. That means after 5 years, a creditor typically can't sue you for the debt. (SOL questions can get fact-specific — if you're near the limit, talk to a Florida consumer attorney to be safe.)

Here's the thing though — and this trips people up all the time — the statute of limitations is completely separate from credit reporting. Two different clocks. The charge-off can still sit on your report for 7 years even if they can't sue you after 5.

Also, if you make a payment on old debt in Florida, you can potentially restart the statute of limitations on the legal side. So if you're going to pay an old charge-off, make sure you understand the timing. And honestly, that's exactly why I tell people to talk to a professional before writing that check — one wrong move and you've reset the legal clock on yourself.

For my clients in Orlando, Kissimmee, Winter Park, Altamonte Springs, Sanford, and across Central Florida, I factor the Florida statute of limitations into every strategy we build.

Frequently Asked Questions

Can I remove a charge-off from my credit report myself?

You absolutely can, yeah. If there are inaccuracies in how the charge-off is reported — wrong balance, wrong date, wrong status — you can dispute it directly with the credit bureaus under FCRA Section 611. Here's where people mess up though (I see this all the time): it's about knowing exactly what to look for and then doing everything in the right sequence. If you pay the charge-off first and THEN dispute, your chances are often better than disputing while you still owe.

Will paying a charge-off remove it from my credit report?

Nope — not by itself. Paying a charge-off changes the status from "Charged Off" to "Paid Charge-Off," but it doesn't remove it. The account history stays on your report. However, paying it off is often a necessary step before you can successfully dispute and remove it — and some mortgage lenders require charge-offs to be paid before they'll approve your loan.

How long does a charge-off stay on your credit report?

Seven years (plus up to 180 days) from the Date of First Delinquency — the first missed payment that led to the charge-off. Not 7 years from when the creditor charged it off, and not 7 years from when you noticed it on your report. If no payment is made by you during that time, it should fall off after 7 years — but you may need to dispute it to force the bureaus to actually remove it.

Should I negotiate the payoff amount on a charge-off?

Absolutely. After an account is charged off, creditors pile on late fees, penalty interest, and other fines — all generated by an algorithm, no human involved. I've seen $300 balances become $700+ from these automated charges. Call the creditor and ask to pay the original amount owed without the added fees. Get any agreement in writing before you pay.

Is a charge-off worse than a collection?

They're both bad, but a charge-off from an original creditor is typically harder to get removed than a collection from a third-party debt buyer. Collection agencies are more open to pay-for-delete agreements. Original creditors almost never agree to delete in exchange for payment. Your best bet with a charge-off is disputing based on reporting errors.

How do I remove a charge-off in Florida?

The process is the same as anywhere — pull your reports, find errors, dispute under the FCRA — but Florida adds a wrinkle. The 5-year statute of limitations on credit card debt means creditors may not be able to sue you after that point, but the charge-off can still show on your report for 7 years. And making a payment on old debt in Florida can potentially restart the legal clock. That's why I always tell my Orlando credit repair clients to understand the Florida timeline before taking action.

Don't Let a Charge-Off Decide Your Future

I've sat across from people in my Orlando office who thought a charge-off meant they'd never buy a home, never get a decent car loan, never breathe easy again.

I'm telling you right now — that's not how this works.

Charge-offs are hard to deal with — harder than collections, harder than late payments. But they don't last forever, and trust me, they can be beaten. You just need the right strategy and you need to execute it in the right order — that's what separates people who get results from people who spin their wheels.

If you're in Orlando or anywhere in Central Florida and you've got a charge-off dragging your score down, call us at (407) 606-7117 or visit contact us today to schedule a free consultation. We'll pull your reports, find the errors, build the strategy, and fight this thing the right way.

Your credit score is worth fighting for. Now let's get in there and throw some punches.

Matt Brody

Founder, Freedom Credit Repair

Matt is the founder of Freedom Credit Repair based in Orlando, FL. With years of experience helping clients remove negative items from their credit reports, Matt is passionate about empowering people to take control of their financial future. Call (407) 606-7117 for a free consultation.